1. What is the Non-Alcoholic Steatohepatitis (NASH) Market Overview – definition, scope, and significance?

NASH is a progressive liver disease characterized by fat accumulation, inflammation, and cellular injury in patients who consume little or no alcohol. The market encompasses diagnostics, therapeutics, and supportive care across hospitals, retail and online pharmacies. Its significance stems from rising obesity, diabetes, and metabolic syndrome prevalence, positioning NASH as a leading cause of cirrhosis and liver transplantation worldwide, thereby driving substantial clinical and commercial interest.

2. What are the key drivers, restraints, challenges, and opportunities shaping the NASH market?

Drivers include escalating metabolic disease rates, unmet therapeutic need, and robust pipeline activity for agents such as Ocaliva and Elafibranor. Restraints involve high R&D costs, regulatory uncertainty, and limited reimbursement frameworks. Challenges arise from heterogeneous disease presentation and the need for reliable non‑invasive diagnostics. Opportunities lie in personalized medicine, combination therapies, and expansion of digital health platforms that enable remote monitoring and adherence support.

3. Which growth trends are currently influencing the NASH market?

Current trends feature a shift toward oral small‑molecule agents, increased adoption of imaging and biomarker‑based diagnostics, and strategic collaborations between biotech firms and big‑pharma. Emerging trends include real‑world evidence generation, patient‑centric outcome measures, and the integration of artificial intelligence to predict disease progression, all of which are accelerating market maturation.

4. How has COVID‑19 impacted the NASH market and what is the recovery trajectory?

The pandemic delayed several Phase III trials and temporarily reduced elective liver assessments, but also heightened awareness of metabolic health. Post‑COVID, clinical activity rebounded quickly, with virtual trial designs and tele‑medicine adoption mitigating earlier setbacks. The market is now on a clear recovery path, supported by renewed investment and accelerated regulatory dialogues.

5. Who are the major competitors and what is the level of market consolidation in the NASH market?

Key players include Intercept Pharmaceuticals, Genfit SA, Novartis AG, and emerging specialists such as BioPredictive S.A.S and One Way Liver, S.L. The landscape shows moderate consolidation, with larger firms acquiring niche biotech companies to broaden their pipeline. Collaborative agreements and licensing deals are common, fostering a competitive but synergistic environment.

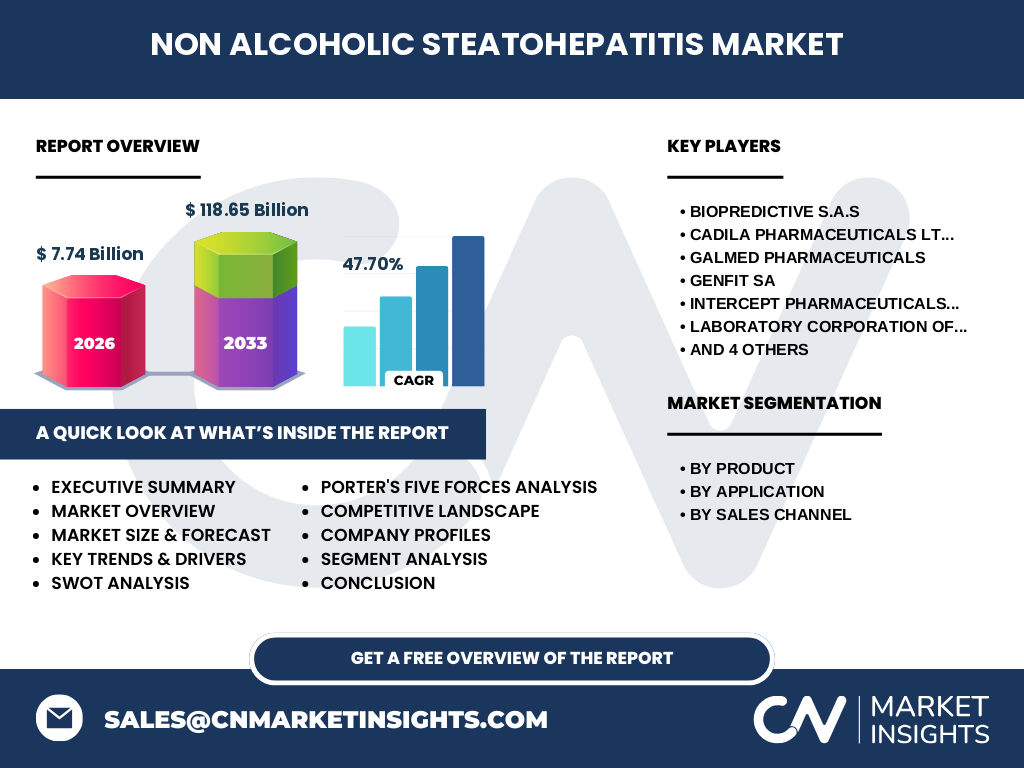

6. What are the high‑level findings presented in the executive summary?

The executive summary highlights a market valued at $7.74 billion in 2026, projected to reach $118.65 billion by 2033, reflecting a 47.70 % CAGR. Strong clinical demand, pipeline diversification, and regional expansion drive growth. Strategic partnerships, innovative diagnostics, and reimbursement advancements are identified as critical success factors for market participants.

7. What are the forecast expectations for the NASH market from 2025 to 2032?

Forecasts indicate sustained double‑digit expansion, propelled by approvals of first‑in‑class therapies and broader insurance coverage. The market is expected to maintain a CAGR close to the historic 47.70 % rate, reaching multi‑billion‑dollar valuations each year and creating sizable revenue streams for both established and emerging companies.

8. How is the NASH market sized and shared by product, application, and sales channel segments?

Product segmentation covers Vitamin E and Pioglitazone, Ocaliva, Elafibranor, and the Selonsertib & Cenicriviroc class. Application is focused on treatment and diagnosis, while sales channels include hospital pharmacies, online providers, and retail pharmacies. Each segment contributes to the overall market mix, reflecting diversified demand across therapeutic and diagnostic solutions.

9. What is the global geographic distribution of the NASH market?

The market exhibits a worldwide footprint, with North America leading due to advanced healthcare infrastructure and robust clinical trial activity. Europe follows, driven by strong regulatory pathways, while Asia‑Pacific shows rapid growth fueled by rising obesity rates and expanding payer access. Emerging economies are beginning to invest in diagnostic capacity, adding depth to the global landscape.

10. How does regional performance vary across the NASH market?

In North America, hospital pharmacy sales dominate, supported by early‑stage drug approvals. Europe displays a balanced split between hospital and retail channels, with strong emphasis on guideline‑driven treatment. The Asia‑Pacific region is characterized by accelerated adoption of online providers and increasing participation in multinational clinical studies, signaling a shift toward broader accessibility.

11. Which companies lead the NASH market and what strategies are they employing?

Intercept Pharmaceuticals focuses on its FXR agonist Ocaliva, leveraging extensive clinical data. Genfit SA advances Elafibranor through combination studies. Novartis AG utilizes its global reach to accelerate regulatory filings. Smaller innovators like BioPredictive S.A.S and One Way Liver, S.L. pursue niche biomarkers and AI‑driven diagnostics, creating complementary growth avenues.

12. What does Porter’s Five Forces analysis reveal about the NASH market?

Competitive rivalry is high, given multiple pipelines and aggressive launch timelines. Supplier power is moderate; raw material sourcing for specialty drugs is specialized but not scarce. Buyer power is rising as payers demand value‑based outcomes. Threat of new entrants is limited by substantial R&D investment and regulatory barriers. Substitutes remain minimal, reinforcing the market’s core demand.

13. What are the SWOT highlights for the NASH market?

Strengths: strong unmet need, high growth potential, and innovative pipeline. Weaknesses: regulatory complexity and cost‑intensive development. Opportunities: combination therapies, digital health integration, and expanding payer coverage. Threats: potential safety concerns, competitive pressure, and uncertain long‑term reimbursement models.

14. How is the NASH value chain structured?

The value chain begins with early‑stage discovery (biomarker identification, compound synthesis), progresses through clinical development, regulatory approval, and manufacturing. Distribution follows through hospital pharmacies, retail outlets, and online platforms, ending with patient adherence programs and post‑marketing surveillance. Service providers such as Laboratory Corporation of America Holdings support diagnostic testing throughout the chain.

15. What investment insights can be drawn for the NASH market?

Investors should prioritize companies with late‑stage assets, diversified pipelines, and strong IP positions. Strategic M&A targeting diagnostic innovators can create synergies. Allocation toward digital adherence tools and AI‑driven patient stratification offers ancillary growth. Monitoring reimbursement policy updates will be essential for risk mitigation.

16. What are the key takeaways from the NASH market analysis?

The NASH market is on a rapid ascent, underpinned by a sizable unmet clinical need and a pipeline rich with novel mechanisms. Geographic expansion, channel diversification, and strategic collaborations are reshaping the competitive environment. Stakeholders who align product development with evolving payer expectations and technological advances are positioned to capture the most value.

17. How was the research methodology designed for this report?

A mixed‑method approach combined secondary data extraction from regulatory filings, peer‑reviewed journals, and industry databases with primary interviews of key opinion leaders, clinicians, and market participants. Trend extrapolation leveraged the provided CAGR and forecast figures, while qualitative insights were validated through cross‑regional expert panels.

18. What is the scope and limitation of this research?

The scope covers global market size, segmentation, competitive landscape, and forward‑looking forecasts up to 2033, focusing on the product, application, and sales‑channel categories disclosed. Limitations include reliance on publicly available financial figures and the exclusion of proprietary company forecasts not disclosed in the source data.

19. Which companies are leading and what recent developments have they announced?

Intercept Pharmaceuticals recently filed for FDA approval of an expanded indication for Ocaliva. Genfit SA announced a Phase III combination trial with Elafibranor and an anti‑fibrotic agent. Novartis AG entered a partnership with Siemens Healthineers AG to co‑develop AI‑enhanced imaging for NASH diagnosis. Smaller players such as BioPredictive S.A.S launched a novel biomarker platform, while One Way Liver, S.L. secured a grant for real‑world evidence collection across European hospitals.